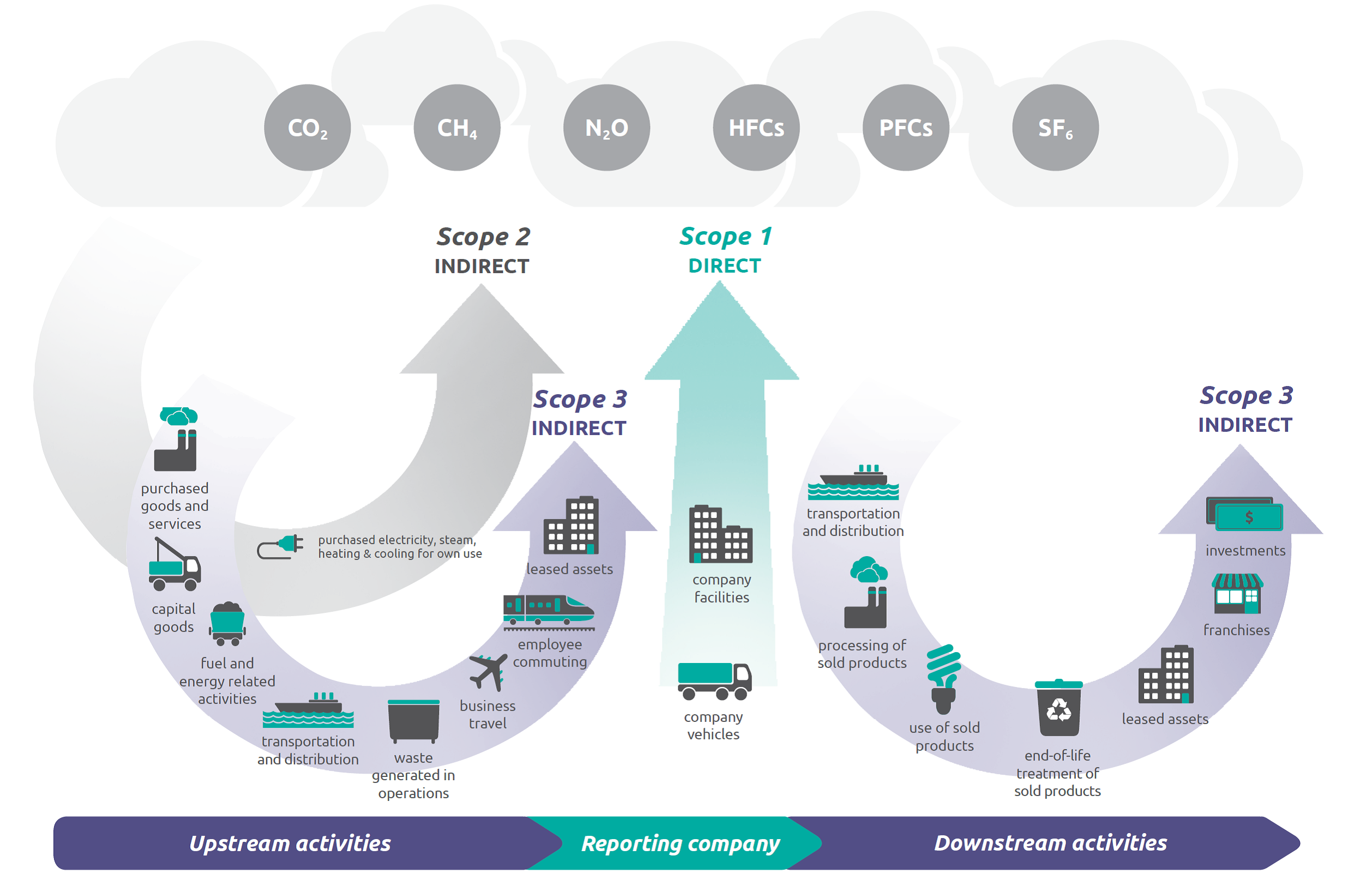

Scope 1, 2, and 3 emissions are ways to categorize where a company or organization’s emissions are coming from. While the first scope comes from direct emissions owned or controlled by a company, Scope 2 and 3 are indirect emissions that come about because of what that company does. These emissions come from sources not owned or controlled by the company.

These categorizations first appeared in the Greenhouse Gas Protocol in 2001, the world’s most widely used greenhouse gas accounting standard. The scopes are a useful tool for businesses to discover and understand their entire value chain emissions so as to put their resources behind the best reduction opportunities.

Scope 1 emissions are the greenhouse gasses that a company or organization emits directly. This can be through company vehicles, fugitive emissions (leaks from equipment or infrastructure), or any emissions from owned or controlled sources.

These emissions are often the first area of focus in a company’s efforts to reduce greenhouse gas emissions as they are the ones it has direct control over.

Scope 1 emissions can generally be further categorized under the following and are dependent on the type and industry of the company:

Fuel combustion from mobile sources

These can come from company-owned vehicles like delivery trucks, service vans, or company cars. Emissions from these sources could also come from heavy machinery like construction equipment.

Fuel combustion from stationary sources

These can come from burning natural gas in company boilers or emissions from diesel fuel back-up generators.

Process emissions

These include emissions from chemical reactions in manufacturing processes, for example cement production, metal smelting, refining operations, iron and steel production, lime production, ethanol production, and hydrogen production (seam methane reforming). All of these produce carbon dioxide (CO2) as a byproduct of their process.

Fugitive emissions

These emissions include the unintentional release of gasses or vapors from industrial activities and processes. They can come from equipment leaks or be released from storage tanks. They are hard to detect and measure, but can contribute significantly to an a company’s greenhouse gas emissions.

Agricultural emissions

These emissions come from agricultural activities and are typically produced by livestock owned by a company or nitrous oxide emissions from fertilizer.

Scope 2 emissions are what a company or organization emits indirectly through the purchase and use of electricity, steam, heating, and cooling. These emissions come from the energy a company consumes. Scope 2 emissions can usually be calculated based on the consumption outlined in energy bills.

Scope 2 emissions are what a company purchases from a utility or other supplier. While the emissions from these sources occur at the facility where this energy is generated, they are attributed to the company that consumes the energy. Scope 2 emissions include:

Purchased electricity

These are emissions produced by the electricity used to power computers, air conditioning, lighting, refrigeration, electronic systems, and cooling systems.

Purchased steam

These are emissions either from manufacturing processes like chemical production and food processing plants, or from heating large buildings.

Purchased heating

These emissions can come from district heating systems which heat buildings from a central source, or boiler systems sourced externally.

Purchased cooling

These can be emissions from air conditioning or refrigeration systems, particular those in supermarkets, warehouses, food processing facilities, data centers, or large commercial buildings.

Scope 3 emissions are a little more complicated. These are the emissions a company or organization is responsible for across its entire value chain. This can be from buying products or services from a supplier, all the way through to when customers use their product or service. Scope 3 emissions are always typically the biggest of the three scopes.

Scope 3 emissions are not directly controlled by a company, but they are a result of its activities. These can include:

Purchased goods and services

These emissions come from the production of raw materials like metals, plastics, and textiles.

Capital goods

This can be from the production of durable goods like machinery, equipment, and buildings.

Fuel- and energy-related activities

These are the emissions from fuels and energy bought by a company that are not accounted for in Scope 1 or Scope 2.

Transportation and distribution

This includes emissions generated by the transportation of raw materials and goods to a company.

Waste generated in operations

These are the emissions caused by waste sent to landfill, recycling, or incineration.

Business travel

Emissions as a byproduct of sending employees on trips via air travel, rail, or car rentals.

Employee commuting

The emissions produced from employees coming to and from work using cars, buses, or trains.

Leased assets

These are the emissions that come from any leased assets by a company not previously included in Scope 1 or Scope 2.

Processing of sold products

These include emissions caused by the processing of sold intermediate products by third parties.

Use of sold products

These are the emissions that come from the use of goods and services sold by a company.

End of life treatment of sold products

These are the emissions that come from the waste disposal and treatment of products sold by a company at the end of their life. This includes the landfilling, incineration, or recycling of those products.

Classifying a company’s emissions into three scopes allows for those companies to better measure, manage, and reduce emissions in a meaningful way. This framework provides a fully comprehensive overview across a company’s entire value chain, meaning that targeted actions can be taken to reduce and eliminate emissions. This is a more holistic approach to emissions management.

This system also means there is clear accountability, as each scope marks out specific areas of responsibility. This again can lead to more effective reduction strategies.

As well, Scope 1, 2, and 3 standardizes emissions reporting so that it is easier to compare emissions data across different organizations and industries.

Each of the three scopes have their own challenges in reducing emissions based in part over the differences in direct control a company has over the emissions sources.

These emissions come directly from the company itself and are the easiest to reduce. Scope 1 can still have its own challenges, however. Changing emission-producing activities like onsite manufacturing processes or owning company vehicles can require major investment in new technologies or equipment and can take years or decades to adopt and implement. In addition, for some industries, there may be limited technological options for replacing fossil fuels with cleaner alternatives

Companies must also consider the operational disruptions with implementing emissions-reducing measures, internal resistance and stakeholder pressure, and uncertainty about future policy regulations.

Successfully addressing these challenges requires a combination of quick wins and longer-term innovation:

Reducing these emissions is slightly more challenging. Even if a company is committed to reducing emissions, it may not have the ability to influence or control how the grid generates electricity, especially in regions where renewable energy adoption is slow, the grid is heavily dependent on fossil fuels, or the infrastructure may not be sufficiently developed to allow companies to reduce emissions quickly.

There are still actions that can be taken to address this. Common strategies include:

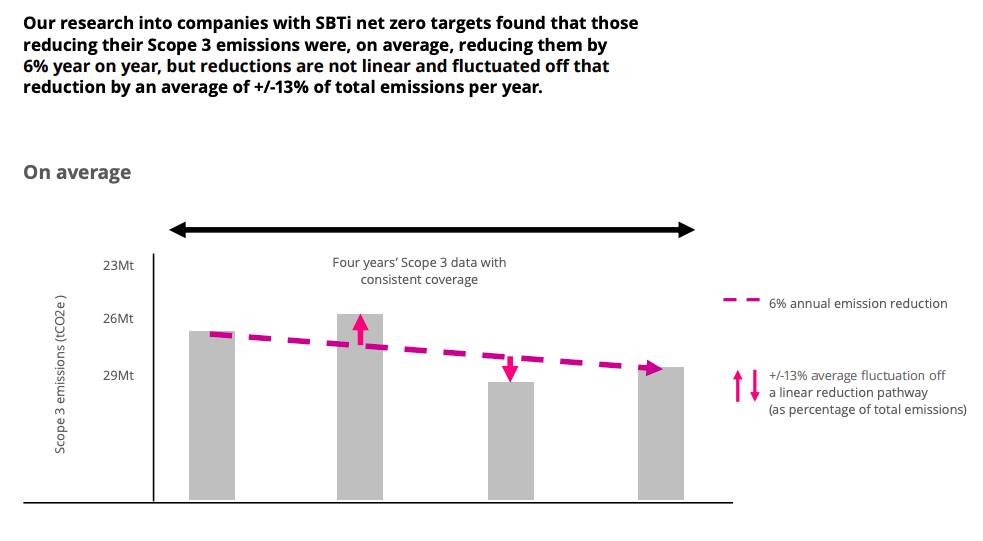

Scope 3 emissions are the most difficult to reduce, as this involves a large and complex range of activities from suppliers to end consumers across an entire entire value chain. This also necessitates collaborating with third-parties which may have different priorities and may not have the financial means to reduce emissions. Getting an accurate data set is also challenging, as it involves a large data collection effort and estimations may have to be made where actual measurements are not possible.

When reducing Scope 3 emissions, companies face high costs and investment requirements, resistance to change, and limited tools for accurate measurement. Additionally, varying regulations, integration with business strategy, and the impact on stakeholder relationships further complicate efforts.

However, companies that successfully tackle these challenges often see significant benefits in terms of cost savings, risk management, and enhanced reputation.

Common strategies to addressing Scope 3 challenges include:

The GHG Protocol Corporate Standard is a widely used framework for measuring and managing greenhouse gas emissions. It was developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD). The standard provides a comprehensive guide for companies to account for and report their emissions, helping them understand their carbon footprint and manage emissions more effectively.

The GHG Protocol Corporate Standard requires companies to report Scope 1 and 2 while Scope 3 emissions are optional but recommended for a more thorough inventory. Additional reporting requirements include:

Base year emissions

This refers to the amount of greenhouse gas emissions produced by a company in a chosen year. Establishing a base year is important as it allows companies to track emissions over time and have a point of comparison.

Emission reduction targets

These are specific emissions reduction goals set by the company. These goals should be trackable and reported regularly.

Data quality and assurance

A company has to show data quality and reliability with internal checks and external verification, as well as explain the methodologies used for calculating the emissions.

Boundary setting

Provide an explanation of the company’s boundaries based on financial or operational control.

Context and transparency

Provide detail reports of where emissions came from and their context, include relevant company policies and management systems.

A greenhouse gas inventory provides an overview of a company’s complete emissions. A well-researched and thoroughly maintained inventory can help set various goals, such as achieving and setting greenhouse gas emissions reduction targets, joining voluntary reporting programs, or achieving greater brand recognition through quantifiable sustainability metrics.

An inventory can be an important tool, but it is not to be confused with emissions reporting, which can be a more detailed presentation of emissions data in required formats set out by the GHG Protocol Corporate Standard.

Calculating Scope 1 emissions means uncovering the total greenhouse gas emissions that come from sources owned or directly controlled by a company. To do so, a company has to:

1. Identify emission sources, which can range from:

2. Collect data of the activity of these emissions sources, which can be done by:

3. Pick an emissions factor to represent the amount of greenhouse gas emitted. Standardized emission factors come from organizations like:

4. Apply the basic calculation formula: emissions = activity data × emission factor

Calculating Scope 2 emissions involves the indirect greenhouse gas emissions from purchased electricity, steam, heating, and cooling. To do this a company has to:

1. Identify emissions sources, which involves tallying up all purchased electricity, heating, steam, and cooling

2. Measure the consumption of all purchased electricity in kilowatt-hours (kWh) as well as the consumption of all purchased steam, heating, and cooling

3. Just as with Scope 2, choose a standardized emission factor.

4. Apply the same formula. For electricity, the formula is electricity emissions (kg CO2e) = electricity consumption (kWh).

Calculating Scope 3 emissions involves measuring all the indirect greenhouse gas emissions that occur within a company’s value chain. These are the most complex to calculate. To do so a company must:

1. Identify emissions sources from these categories defined by the GHG Protocol:

2. Collect data of the activity of these emissions sources. This is similar to step 2 for Scope 1 emissions but is more thorough.

3. Choose an emission factor.

4. Apply the same calculation formula: emissions = activity data × emission factor.

The future of Scope 1, 2, and 3 emissions will likely focus on more stringent reduction targets and comprehensive strategies as businesses and governments intensify efforts to combat climate change. Innovations in technology, such as cleaner energy sources, improved efficiency, and advanced carbon capture, will play a key role. Companies will increasingly need to address Scope 3 emissions, involving broader value chain engagement and collaboration. There will be a growing emphasis on transparency, with enhanced reporting and verification requirements to ensure accurate tracking and accountability. Overall, reducing all three scopes will be crucial for meeting global climate goals and achieving net-zero emissions.

Measuring Scope 1, 2, and 3 emissions provides a comprehensive view of a company's total greenhouse gas impact, supports regulatory compliance, and helps identify risks and opportunities. It enables strategic planning, enhances corporate reputation, and drives competitiveness by meeting stakeholder expectations. Accurate measurement also aids in setting and tracking sustainability goals, improving efficiency, attracting investment, and fostering innovation.

Direct emissions are greenhouse gases emitted directly from sources owned or controlled by a company, such as fuel combustion in company vehicles or emissions from on-site industrial processes. Direct emissions fall under Scope 1. Indirect emissions, on the other hand, are those that occur as a result of the company’s activities but come from sources not owned or controlled by the company itself. These include emissions from purchased electricity (Scope 2) and emissions from the broader value chain, such as those from suppliers or product use (Scope 3). Essentially, direct emissions are under the company’s direct control, while indirect emissions are associated with its broader operational impact.

Upstream and downstream emissions are two categories of Scope 3 emissions. Upstream emissions are the greenhouse gases released during the production and supply of goods and services before they reach a company, including raw material extraction, manufacturing, and transportation to the company. Downstream emissions occur after the company's products or services have been delivered, covering the emissions from product use, end-of-life disposal, and distribution to consumers.

Scope 4 emissions are not part of the official GHG Protocol classification but are increasingly discussed in the context of sustainability. They refer to the avoided emissions that result from a company's products or services that help reduce emissions elsewhere in the economy. Essentially, Scope 4 emissions are the positive impact or reduction in emissions achieved due to the use of a company’s products or services, which offset or avoid emissions that would have otherwise occurred.

For example, if a company produces energy-efficient appliances, the emissions avoided by consumers using these appliances (compared to using less efficient alternatives) could be considered Scope 4 emissions. This concept highlights the potential benefits of products and services in contributing to overall emission reductions beyond the company's direct and indirect operations.

Scope 1 and 2 emissions reporting is often required by regulations in many regions, especially for large or certain industries, as part of environmental or carbon accounting mandates. Scope 3 reporting, while less commonly mandated by law, is increasingly encouraged through sustainability frameworks and investor expectations, reflecting a broader push for comprehensive environmental disclosure. Overall, there is a growing trend towards both mandatory and voluntary reporting of all three scopes of emissions to meet regulatory requirements, investor demands, and sustainability objectives.

Decarbonization is crucial to safeguarding the future of our planet, as it ...

We need carbon accounting to quantify and manage greenhouse gas emissions, ...

Carbon neutral and net zero are two terms often used interchangeably, but t...